A Web of Deceit? State Pension Funds and Non-Profit Foundations Investing in Activist Hedge Funds

The aims of activist hedge funds may seem harmless, even virtuous. But who are they really benefiting? Growing evidence suggests that the only true winners are the billionaires who run these funds. So why are public pension funds – some supported by taxpayer dollars – investing in these instruments of economic destruction?

Research indicates that state pension funds have invested in activist hedge funds. Public records show that New Jersey’s pension fund has investments in the activist funds Starboard Value and Jana Partners. Florida’s pension fund also has invested in Starboard Value.

Governor Ron DeSantis’ role as chair of the pension fund makes him a Wall Street player of sorts, as evidenced by his recent comments about Elon Musk’s buyout of Twitter – which were followed by Musk’s sudden, and not necessarily coincidental, conversion to the Republican Party.

Even nonprofit foundations established to benefit society are lending support to these predatory activist investors. Are the Ford Family Foundation, the Dr. Scholl Foundation and the Edward & Sandra Meyer Foundation aware of what’s being done with their money? The fact is that when activist hedge funds pounce on a company, the result tends to be disastrous for everyone but the activists: poor long-term returns for shareholders and a loss of jobs for employees.

Billionaires’ Delight

The activist sales pitch seems compelling at first. Replacing an apparently lackluster board with new thinking – and lighting a fire under management – which may seem like a good way to boost shareholder value.

But it’s increasingly clear that activist hedge funds are the successors to leveraged buyout specialists of a generation ago: quick-buck seekers operating out of their own, usually short-term interest. So when a prominent activist hedge fund like Starboard Value goes after a dizzying array of companies in a matter of months – including Huntsman, GoDaddy, Papa John’s, Commvault Systems, Kohls, LivePerson, eHealth, On Semiconductor, ACI Worldwide, Aecom, Cerner, Elanco Animal Health, Merit Medical Systems, Onyx Acquisition, and Warburg Pincus Capital – alarm bells should be ringing for their shareholders and employees.

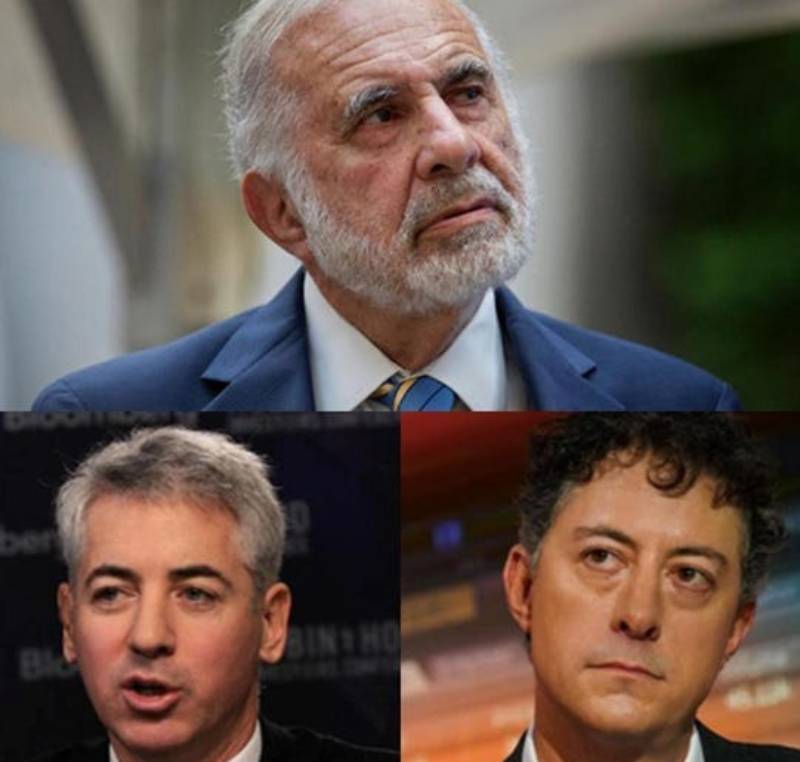

It’s no coincidence that some of the largest activist funds are run by multi-billionaires: Carl Icahn of Icahn Capital Management (net worth $16.7 billion in mid-May 2022, according to Forbes), Paul Singer at Elliott Management ($4.3 billion), Daniel Loeb of Third Point ($4.2 billion) and Bill Ackman of Pershing Square Capital Management ($2.9 billion).

Activist investors like these are out to turn a fast profit – the polar opposite of the long-term commitment it takes to build a thriving company with a healthy culture that serves customers, employees, shareholders, and other stakeholders. For these billionaires, the quickest path to a short-term windfall comes from slashing costs to attract a company sale. That’s bad for three reasons.

First, selling the company to a competitor or a private equity firm isn’t always in the best interests of customers – who lose the ability to choose among competing providers of goods and services – or employees. And it rarely serves the country’s need for dynamic markets that foster innovation and entrepreneurial energy.

Second, drastic cost-cutting usually means layoffs and corner-cutting that lowers employee morale and customer satisfaction. Cost-cutting can also mean abandoning ongoing investments in new products or markets that have yet to bear fruit but are essential for the company’s long-term prospects. In fact, one study showed that the average company taken over by activists suffers a 50% drop in research & development spending during the time the hedge fund is in charge.

Third, a recent study also showed that companies targeted by activist hedge funds tend to be poor corporate citizens, finding that “as soon as an activist hedge fund takes ownership of a company’s shares, the company is likely to firmly place on hold their efforts to be more environmentally sustainable and socially responsible.”

The bottom line is that shareholders don’t do well, either. The same study found that after a short-term uptick in company value, “the value of the companies targeted by activist hedge funds steadily drops [and continues] downwards five years after targeting.” That’s why it’s troubling that state pension funds and some philanthropic nonprofits support these activities. Does Gov. DeSantis really think his populist image will be helped by associating with activist funds that lay off workers and handicap companies?

Short-term benefits for billionaires, long-term losses for employees, shareholders, and society. Seems like a very raw deal.